AI In Banking Has Outgrown The Chatbot Label

At a glance

- “AI in banking” is an umbrella term. RPA, machine learning, and conversational AI solve very different problems.

- One of the most common buying mistakes is treating rules-based bots and conversational AI agents as the same category.

- The most practical split for CX initiatives is autonomous agents (serve customers) versus copilots (assist employees).

- If a bank doesn’t define the job-to-be-done first, it can buy “AI” and still end up with queues, rework, and compliance risk.

The trouble with "we need AI" for banks & credit unions

Banks and credit unions may say they “need AI”, but that statement can be about as indefinite as saying they need “software”.It’s directionally correct, yet operationally vague.

In practice, “AI in banking” covers a wide range of technologies—from automation in the back office to conversational systems that interact directly with customers. These systems typically fall into three categories: robotic process automation, predictive analytics powered by machine learning, and conversational AI.

Understanding the difference between them is what turns an AI strategy into an actual operating plan.

What “AI in banking” actually includes

Most banking AI roadmaps combine three distinct technology categories:

RPA

Robotic process automation handles repetitive, rule-based tasks. Examples include form processing, document routing, and simple workflow steps that follow fixed logic.

RPA is extremely effective for structured internal processes, but isn’t designed for conversations or customer interaction.

Traditional analytics and machine learning

Machine learning systems focus on prediction and detection. Banks use them for credit scoring, fraud detection, risk analysis, and portfolio monitoring.

These models analyze patterns in large datasets but typically operate behind the scenes rather than interacting directly with customers.

Conversational AI

Conversational AI systems interact with people using natural language through voice or chat interfaces. These systems can handle multi-turn dialogue, interpret intent, and carry context across a conversation.

If your objective is to reduce contact volume, improve resolution rates, or provide service outside business hours, conversational AI is usually the relevant technology category.

Stop lumping deterministic bots and conversational agents together

Many banking teams still treat chatbots and conversational AI as interchangeable. In reality, they represent very different technologies.

Deterministic bots operate using predefined rules and scripted responses. They work reasonably well for simple FAQs or menu-style interactions but tend to fail when customers phrase questions differently or introduce new context.

Conversational AI agents operate more like dialogue systems.They interpret intent, maintain context across multiple turns, and adapt responses dynamically during a conversation.

The practical implication is important. A bank that says “we tried chatbots and they didn’t work” may have only experimented with deterministic scripts. That experience doesn’t necessarily reflect how modern conversational AI agents perform.

Autonomous agents versus copilots: the decision that matters

A more useful way to think about banking AI is to ask who the system is designed to serve.

- Autonomous agents interact directly with customers. They can handle routine service requests, conduct account notifications, or manage outreach for payment reminders.

- Copilots assist employees rather than replacing interactions. They surface knowledge, recommend responses, summarize conversations, and accelerate workflows during calls.

This distinction is often the most helpful way to scope an AI pilot.

If the goal is to eliminate wait times or absorb large volumes of routine requests, autonomous agents usually make sense. If the goal is to improve agent productivity or consistency without changing the customer-facing channel, copilots may be the better starting point.

A buyer’s checklist that prevents predictable failure

Before selecting an AI platform or vendor, banks should answer a few operational questions.

- First, define the job clearly. Which intents or workflows are in scope, and which ones are intentionally excluded?

- Second, confirm whether the system can actually execute work. Some solutions can answer questions but can’t authenticate users or perform account actions.

- Third, ensure auditability. Regulated communications require transcripts, logging, and policy enforcement mechanisms.

- Fourth, design escalation paths. Teams need to define when and how conversations transfer to human agents.

- Finally, establish measurement upfront. Containment rates, resolution outcomes, and error modes should be defined before deployment, not after.

Skipping this groundwork often leads organizations to purchase an impressive demo rather than a system that can run reliably in production.

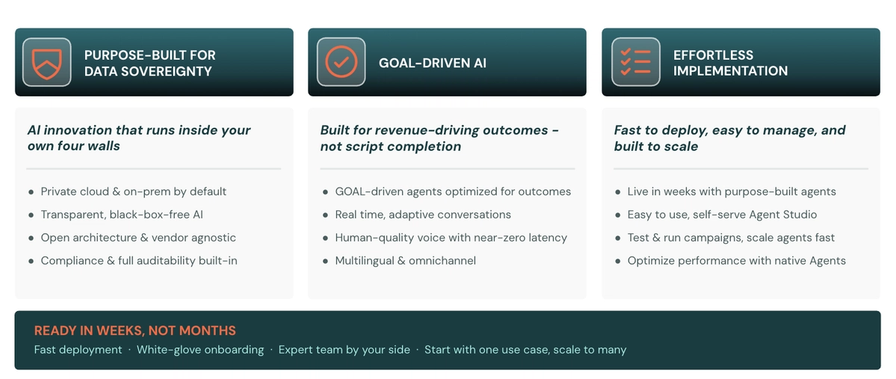

How Acclaim helps

Acclaim is designed for the conversational layer of banking AI—specifically, where institutions need systems that interact directly with customers.

Its GOAL-oriented AI agents are built to complete defined banking tasks such as resolving support requests, delivering account notifications, or conducting payments reminders. Instead of open-ended chatbot conversations, each interaction is structured around a clear business outcome.

Acclaim also provides auditability and compliance controls required for regulated communications, including transcripts, policy enforcement, and configurable escalation paths.

The result is conversational AI that moves beyond scripted chatbots and operates as a reliable operational layer within banking customer experience.